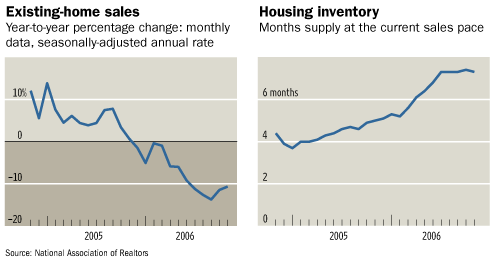

Canada could be headed for a housing and mortgage meltdown similar to the one that has devasted the U.S. economy, Merrill Lynch warned Wednesday.

Canadian households are more financially overextended than their counterparts in the United States or Britain, a report issued by Merrill Lynch Canada economists David Wolf and Carolyn Kwan says.

So it's revealed that Canadian home owners have more debt than their US or British peers. How comforting.

“What worries us is that Canadian households have been running a larger financial deficit than households in either the U.S. or the U.K.,” the Merrill report says. “... After 40 years of net saving, Canadian households moved into sustained deficit in 2002. In 2007, household net borrowing amounted to 6.3 per cent of disposable income, a wider deficit than in the U.K. and not far off the peak U.S. shortfall seen in 2005.”

But yet many still believe we are different.

To read David Wolf's full report, "The Tipping Point," click here.

Update:

Perhaps the Merrill Lynch report has ruffled a few feathers among other economists (are they speculators themselves?).

The nature of the decline in Canada is much different than that of the

U.S., said Benjamin Tal, senior economist at CIBC World Markets Inc.

"You need a trigger for a crash in the housing market. In 1989 to

1990, the trigger was double-digit interest rates that killed affordability in

Canada. In the U.S., the trigger was subprime, and a huge increase in default

rates when people who were not supposed to be in the business of owning a house

did, and that created artificial demand," he said. "Unless Canada goes into a

major economic recession ... I'm missing that trigger."

Let me do your job for you.

Falling house prices. That is the trigger. It's simple.

40 year mortgages, 0 downpayment, etc...all these new mortgage products introduced by the CHMC over the last two years force-fed false affordability on unsuspecting home buyers. These are the same home buyers that would not even qualify for a traditional 25 yr amortization period. People who have no business buying houses bought during the last two years. Just talk to my single hairdresser who owns 3 properties. A significant majority of homes bought in the last two years were bought with 40 year mortgages. Once can argue that affordability is now worse in 2008 than it was back in the 1990s as now the principle amounts of mortgages are astronomical.

In the US, the trigger was not subprime. Subprime would have never been an issue if house prices continued to rise or remained static. Those who were overextended once the teaser rates adjusted to higher rates could easily escape by either selling their property or refinancing their mortgage. When house prices fell in the US, those home buyers with subprime mortgages were trapped. They couldn't sell because there were no buyers. And they could no longer refinance their mortgages because their property was losing significant value. The only option was to default.

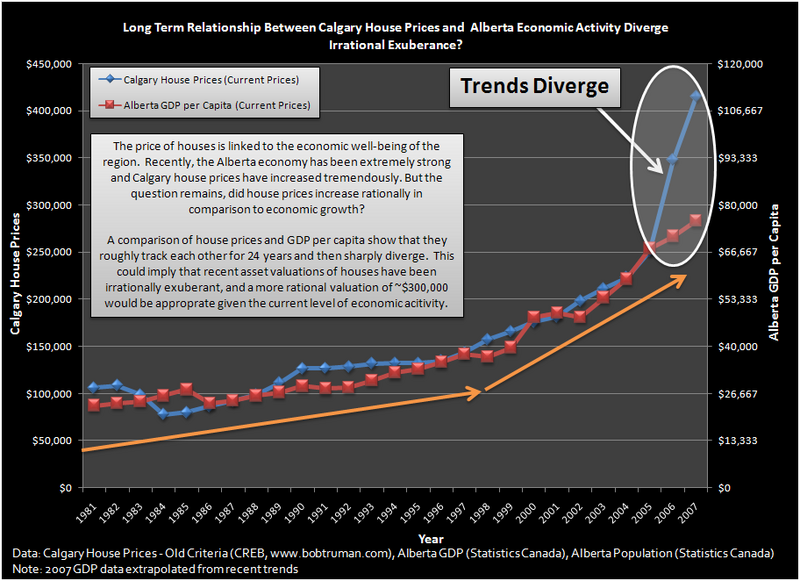

The same scenario is occurring in Calgary and other cities across Canada. Houses aren't selling under similar principles. I fear that sellers are unwilling to lower their prices because they will take a big loss. Intelligent buyers, are exercising their patience on the sidelines. Meanwhile, home prices which have risen exponentially over the last two years are starting to come crashing back down. Soon many Canadians will be in the same trap. Severely upside down on their mortgage they will be forced to either sell or refinance their mortgage. Both of which cannot be accomplished when asset values are decreasing. Skyrocketing inventory is a symptom and precursor of what is to come.

Reality check, as house prices slide in every major Canadian city - real estate is still unaffordable to the average wage earner. These include important people such as teachers, firefighters, nurses etc.

Even if our own meltdown is a fraction of what happened in the US, it will still have a significant impact on our own economy. Perhaps an in-house grown recession (pun intended).

To simply ignore all the warning signs and to discount what is happening in the US is complete ignorance.

In addition,

In addition,

We're almost approaching the midway point of 2008. With the spring rush come and gone, will the following bold predictions hold true till the end of the year?

We're almost approaching the midway point of 2008. With the spring rush come and gone, will the following bold predictions hold true till the end of the year?

The much anticipated "spring rush" has been a complete disaster in Calgary's real estate market. This is well documented in the

The much anticipated "spring rush" has been a complete disaster in Calgary's real estate market. This is well documented in the

The once white-hot Calgary real estate market boasted a vacancy rate of 0.5% back in 2006. According to this

The once white-hot Calgary real estate market boasted a vacancy rate of 0.5% back in 2006. According to this

{kind=link}