Real Estate Type : Single Family

Building Type : House

Bedrooms : 1

Bathrooms : 1

Interior Floor Space : 925.70 sqft

Storeys : Bungalow

Built in : 1926

Land Size : W:8.840m D:36.580m Shape:REC

Title : Freehold

Location : 112 9 Av NECalgary, AB T2E 0V2

MLS®: C3322995

Aren't post grow-op properties supposed to be a good deal?

This is more evidence that the Calgary real estate market is out of touch with reality. The seller of this property is looking for $320k for a post grow-op establishment. The house is most likely extensively damaged and is currently being evaluated by the Calgary Health Region. The MLS listing makes reference that the purchase would be more land motivated (even though the lot is in an ambiguous location).

It's still astonishing to see the level of denial that still exists in the marketplace.

Here Is What $320k Will Get You

Monday, May 26, 2008

Bullish Hopes Sputtering

Sunday, May 18, 2008

Chicken soup won't help. Not doom and gloom but rather reality.

Calgary inventory at all time record highs (7127 SFH + 3373 Condo), sales/new list ratio in the tank, sales down yoy 30%-50%, median price down yoy, average price down yoy, days on market up yoy.

As of May 16, 2008 there are 10500 properties on sale, sacrificial offerings from many financial tight rope walkers who are losing balance. Sellers are in a mixed progression mode from fear, desperation and panic. Capitulation soon to follow this summer when sales are further reduced as stressed out Calgarians partake in $ummer vacation$ and the $tampede. The financial arithmetic no longer computes in purchasing real estate in Calgary, unless the "low ball" technique is engaged. Yet, there are still a few suspended in a perpetual state of denial - hoping.

"I'm standing my ground on this one. There is no subprime lending in Canada even remotely similar to that in the USA. Not even close!"

The great hope that we avoided the same pattern of lending as seen in the US. But in Canada, we have our own diseases. 0 down, 30, 35, and 40 year mortgages are just some typical examples of unconventional lending practices (ticking time bombs)recently introduced in the market in the last two years. Not covered is the potential of higher mortgage rates in the future. As house prices plateau and soon decrease, buyers who forced affordability will face impending financial apocalypse. Again, not an overnight phenomenon. One that will present itself gradually over time.

"There is a good possibility that many of these buyers will be coming from Ontario and Quebec."

The great hope of a locust-style provincial invasion of laid off Eastern workers. The seller loses all focus and care for human condition. Forget the sheer emotional drain of losing your livelihood. Come to Alberta, so specuvestors can unload their ill advised lifetime debts. The hope of naivety, that is their goal. But this story has been written before and the ending resulted in net negative migration away from Alberta in late 2007 and early 2008. What will be different this time around? Nothing. If positive migration occurs it will be once again temporary. The top priority of a laid off employee is not home buying. Is the labour shortage in Alberta more of a function of net negative migration (high cost of living) or a booming economy?

"The gloom and doom prognostications predicting a correction as in the U.S. will not come into fruition as long as oil is over 100 USD."

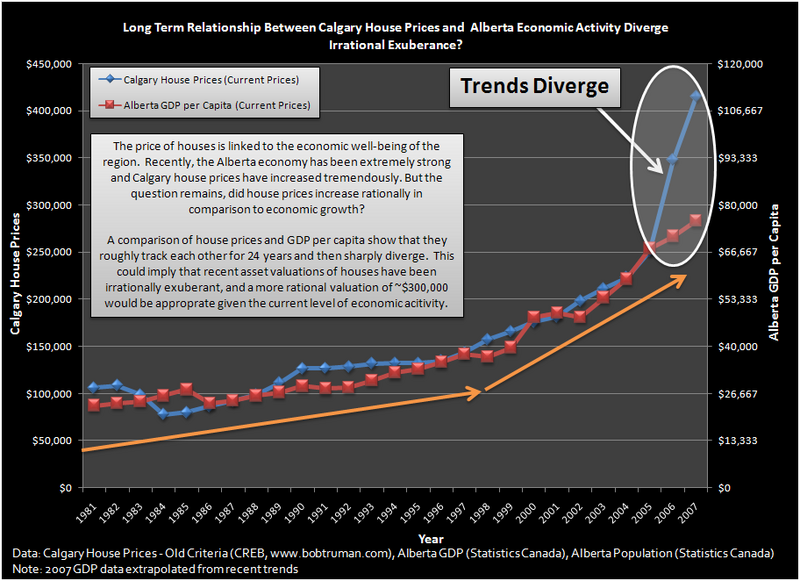

The empty validation that if oil is at a high price, the world is fine. This topic as been beaten to death, revived and beaten to death yet again. Bloggers on the Alberta Bubble Blog have empirically concluded there is no direct relationship between the two variables. As per Radley77, there is a divergence of Alberta's GDP versus the recently increase in house prices. Only the naive still believe that Calgary's house prices are sustained by oil and gas. The high price of oil is a result of hedging against the dropping value of the greenback. High price of oil favours no one. Peripheral expenses will increase as a function of this. Transportation costs become more cost intensive, food production costs increase, etc. Disposable income is further stripped away from already debt-ridden Calgarians. High prices translate in to reduced demand (humans will adapt). Oil was a false validation that the real estate marketing machine integrated in their campaign in the recent years to "fog" and "bait" buyers.

Bold Predictions

Thursday, May 15, 2008

We're almost approaching the midway point of 2008. With the spring rush come and gone, will the following bold predictions hold true till the end of the year?

We're almost approaching the midway point of 2008. With the spring rush come and gone, will the following bold predictions hold true till the end of the year?

Here is a compilation of predictions for the Calgary real estate market made at the beginning of this year. Keep in mind, some of these predictions seem formulated with an absence of supply-demand economic fundamentals (severely weakened sales and record high inventory).

"Jan 30

It speaks to the amazing strength of the Calgary economy that in spite of decreased sales and increased inventory, the price is remaining stable, or even rising slightly. If prices stay where they are now, and I fully expect them to, within a +/- 5% range, the buyers will appear. People have been waiting to see what would happen in January and now they know. My phone is busy, and many other realtors I've talked with, report plenty of interest. Sales will be down considerably this year compared to the frenzied activity of 2006 and 2007, but it seems to be a non-issue. When you compare this year's sales to the years when we had a normal balanced market, we're right on the average.

Will my prediction come true?

I predicted on Jan 30 that Single Family Home prices would fluctuate this year within +/- 5% of the January price. That would mean we could see a drop in median prices to as low as $389,500, and average price to $432,532."

-Bob Truman, First Place Realty (source: What's New Section)

"The average sale price of a single-family home in the city will flirt with the half-million-dollar mark this year, according to the Calgary Real Estate Board.

In its 2008 forecast Wednesday, real estate board president Ed Jensen said the MLS average will increase by five per cent this year to $495,800 while condominium prices will rise by six per cent to an average of $335,300.

Total sales will dip by five per cent for both the condo and single-family markets, to 7,700 and 17,500 respectively, compared with 2007."

-Ed Jensen, President of CREB (source: Calgary house prices to inch toward $500,000)

"We're looking at about 5.5 per cent moderation in MLS sales and our price growth is in the same ballpark. We're looking around the 3.5 to five per cent level, too," said Louie. "There is a lot of supply out there. Going into the last part of the year we saw demand ease off. Some of that was because of the higher prices, but also there is a lower level of net migration that we're seeing coming to Alberta."

-Lai Sing Louie, senior CHMC Calgary market analyst (source: Calgary house prices to inch toward $500,000)

"And in the long-term, real estate here looks great, says Campbell, adding year-over-year average house price gains in Calgary should be in the 11 per cent range this year."

-Don Campbell, President of REIN Canada (source: Is housing influenza infecting Calgary?)

Update:

"The CMHC's Spring 2008 Calgary Housing Market Outlook, released Thursday, said the average residential price for a resale home in the Calgary census metropolitan area will hit $429,000 this year (3.6% increase), increasing from $414,066 in 2007.

The average price is forecast to climb to $450,000 next year.

...

The CMHC said MLS sales will decline by 19.2 per cent this year from 32,176 in 2007 to 26,000, but sales will rebound in 2009 with a 2.9 per cent increase to 26,750.

Also, new listings in the resale market are expected to rise by 14.4 per cent this year to 62,000 from 54,202 in 2007. But they will drop by 9.7 per cent in 2009 to 56,000."

-CMHC's Spring 2008 Calgary Housing Market Outlook (source: Housing gains take breather)

False Sense Of Affordability

This might be old elementary news, but over the last couple of years during the inflation of the Calgary real estate bubble many home buyers were "tricked" (yes, I dare say it) into affordability.

A conventional and financially rational mortgage would follow a 25 year amortization period. A down payment requirement of 25% would be a solid foundation. In addition, a single income stream would the norm.

Since February 2006, CHMC has introduced 30, 35 and 40 year mortgages to allow prospective buyers a chance into the real estate market. In conjunction to low interest rates, a well oiled real estate marketing machine, and a booming economy this created the present bubble dynamic.

Recently, the essence of 40 year mortgages has been questioned.

"Canadians are flocking to 40-year mortgages, often without a down payment, and the rapidly developing trend is beginning to ring alarm bells for policy makers in Ottawa.

Both the Finance Minister and the Governor of the Bank of Canada are expressing concern about the situation, as the U.S. economy continues to reel from a crisis triggered by mortgage holders who were in over their heads."

The shocking statistic found in the article is that around 40% of new mortgages are of longer than conventional 25 year periods. Furthermore, 15%-20% of first time home buyers are opting for no down payments and 40 year mortgages. Since Calgary lead the sudden incline in prices, unconventional lending practices may be more pronounced in the market.

Instant applications to a life of serfdom and financial tight rope walking. Longer term mortgages cost thousands more just in paying interest and last much longer. They are only beneficial to your bank, mortgage broker and anyone in the real estate "money supply chain."

"The bigger question is what happens as you go off two, three, four, five years from now, and it's no longer just a significant share of the new applications, but it's a significant share of the outstanding market," said Derek Holt, an economist at Bank of Nova Scotia. "I think we'll be in uncharted waters as to the sensitivity to shocks that most households will find themselves facing." If there is a shock in jobs, interest rates or commodity prices, "unless you see the arrival of 60-year mortgages, then you've got a household sector that's really backed itself up against the wall."

If the current state of affordability is defined as minimal down payment on a mortgage longer than 25 years, the cold reality is much different. You can't afford the house (wait for the price correction).

The most dangerous lifetime financial decision is "force feeding" affordability in a bubble real estate market.

Offending Economists Around The World

Thursday, May 8, 2008

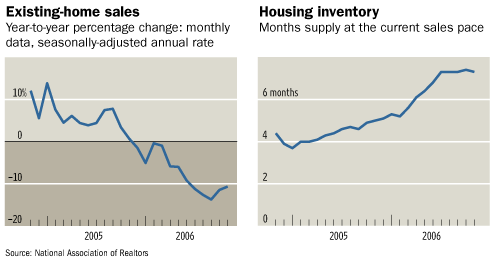

The preceding graphic was the housing market in the US where prices eventually crashed. Early symptoms included a decrease in sales and high inventory levels.

Notice the very "shocking" similarities to the trend of the Calgary real estate market. In Calgary, home sales are plummeting 30%-40% YOY. Inventory has risen to all time record highs (~7000 city SFH, ~3200 city condos). By exhibiting the same symtoms, it seems that the Calgary real estate market will suffer the same illness.

According to this article, CREA is forecasting the resale market in the province will drop by 18.9 per cent to 57,900 units this year and experience a further five per cent drop in 2009 to 55,000 MLS sales. Interesting to note, the report says the average sale price in Alberta will rise by 4.7 per cent to $373,000 while it will only go up by 2.8 per cent in 2009 to $383,300.

So how exactly does retracting sales contribute to rising prices?

As a commodity, real estate is rather complex. But don't be fooled, real estate is still bound by the same simple economic fundamentals of supply and demand. The price function isn't perfectly elastic (but rather "sticky"), therefore price fluctuations will take more time to develop.

This type of reporting should be insulting to any economist. By CREA's estimation, economists around the world should be going back to their post secondary institutions and demand for refunds on their educations. Adam Smith is rolling twice over in his grave. Insulting the intelligence of the common person will only cause CREA and its members to further lose credibility.

Contrary to real estate perma-positive pumping reports, increasing inventory and decreasing sales will reduce property prices.

It's inevitable.

More Negative Equity On The Horizon

Saturday, May 3, 2008

The much anticipated "spring rush" has been a complete disaster in Calgary's real estate market. This is well documented in the MSM these days. It was during this period that sellers were hoping to unload their anvils of debt to unsuspecting greater fools. The hope and anticipation were met with retreating buyers. In analyzing historical trends, sales should dwindle further during the next coming summer months propagating further price declines.

The much anticipated "spring rush" has been a complete disaster in Calgary's real estate market. This is well documented in the MSM these days. It was during this period that sellers were hoping to unload their anvils of debt to unsuspecting greater fools. The hope and anticipation were met with retreating buyers. In analyzing historical trends, sales should dwindle further during the next coming summer months propagating further price declines.

In July 2007 we saw the peak for Calgary SFH market hit an average price of $505,920 and median price of $439,000 (achieved in June 2007). This was followed by months of declining prices. The year ended in December 2007 with an average price of $444,769 and a median price of $406,788. Summer buyers would already owe more on their mortgage loans than the value of their homes.

Suffice to say, we may start seeing month-over-month price declines as early as this month. This means the price declines will be longer and more painful for sellers this time around. With inventory at record levels and low sales, the price declines this year will be magnified.

By the end of this year, there is potential that a high percentage of home buyers during the last two years will in a negative equity position. Negative equity, an element in the real estate game that your friendly real estate "professional" did not address during the frenzied buying hysteria. But is has now become a reality for most home owners in Calgary. In combination with being "house poor," many bubble buyers will be in a constant state of financial duress. This may mean not having enough money to send your real estate "professional" a Christmas card this year.

As negative equity builds, market exit strategies for sellers are minimized and financial losses will be greater.

Those who are overextended could possibly tip the rest of the market into a severe correction.

...

A new reality in Calgary. Overextended homeowners will use creative ways to find tenants to help cover mortgage costs on multiple homes.

{kind=link}